Read More

Eric Tsang and his daughter pocket 8pc profit on The Cliveden home sale

23-06-2026 15:13 HKT

Human skull found hanging from tree on Round Island near Chung Hom Kok

24-06-2026 01:50 HKT

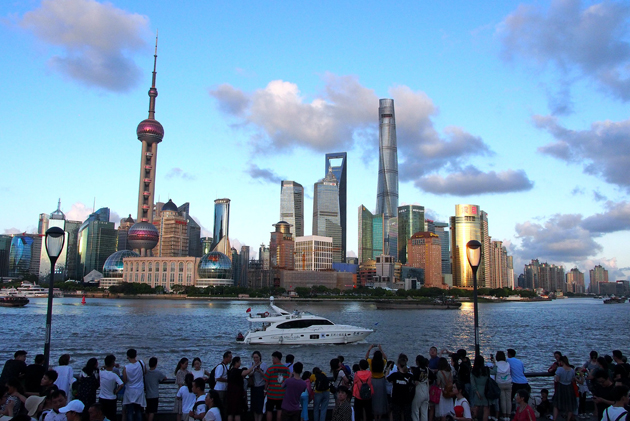

Reports that the Chinese regulator has barred domestic brokers and their overseas units from opening new offshore trading accounts for mainlanders could not be more untimely for Financial Secretary Paul Chan Mo-po.

News of the ban - first reported by Reuters and then the Financial Times and Bloomberg - broke as a group of experts named by Chan came under pressure to produce a report in time for the policy address to include measures to enhance liquidity of the city's financial market.

It looks like that the experts will have to remove options from their draft if they ever considered drawing on mainland investors to trade in the local market with a view to enriching market liquidity that has contracted from a daily trading average of HK$166.7 billion in 2021 to HK$112 billion this year and, occasionally, below HK$50 billion a day.

Sympathy goes to the financial secretary as his hands are tied tighter.

The reported ban, if confirmed eventually by the mainland, is bound to reduce the choices available to Hong Kong as it seeks to reboot its financial market.

According to the reports, domestic brokerages and their overseas units are prohibited from taking on new mainland clients for offshore trading.

Worse still, new investments by existing mainland clients are also affected as they would be subject to a "strict monitor" to prevent investors from circumventing the mainland's foreign exchange controls.

It is common knowledge that mainland investors use Hong Kong the most for offshore trading.

In other words, Hong Kong may have also become a major channel for the mainland's rich to get their capital out of the country via offshore trading, over which Hong Kong can only claim innocence as it practices a free economy and has no foreign exchange controls.

After the mainland halved the stock stamp duty earlier to stimulate trading, calls mounted here for the financial secretary to follow suit.

Chan has been reluctant to do so and is now vindicated for his reluctance after mainland stocks, dragged down by investors' fears over major Chinese real estate developers' successive defaults on debts, continued to perform poorly despite the stamp duty cut.

Chan was right to note that lowering the stamp duty cannot stimulate trading long term. Rather, it is about investors' faith in the economic outlook - and this depends on economic performance, company earnings, political atmosphere, among other factors.

However, these are also tied to the amount of money that investors may park in Hong Kong.

Following the ban, previously consented activities - including cross-border securities broking, securities lending, fund sales and investment consulting - it has become illegal for these services to be offered to clients from the mainland.

Chan and the group of experts will have to reveal their recommendations very soon as Chief Executive John Lee

Ka-chiu will deliver his policy address later this month.

Reports that the China Securities Regulatory Commission has told brokers to stop offering securities trading from offshore accounts such as Hong Kong to new mainland investors threatens to deal their efforts an accidental blow.