Read More

Taxi e-payment ‘3pc fee’ notices spark debate on rollout day

02-04-2026 12:42 HKT

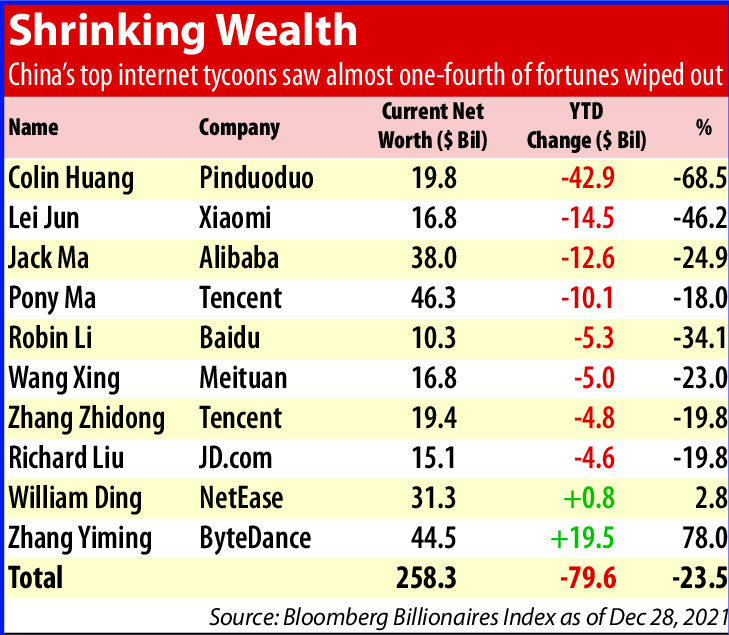

The country's 10 richest tech tycoons lost US$80 billion (HK$624 billion) in combined net worth in 2021 amid widescale crackdowns by Chinese regulators.

Pinduoduo founder Colin Huang lost the most this year - US$42.9 billion, or two-thirds of his fortune - as shares of the e-commerce platform plunged nearly 70 percent. Alibaba's Jack Ma Yun, who has been keeping a low-profile since authorities clamped down on his sprawling business empire, has seen his wealth cut by about US$13 billion.

The euphoria was short-lived. The Beijing-based company's shares have plummeted more than 60 percent since Chinese officials announced an investigation and asked it to delist from the New York Stock Exchange, leaving Cheng's fortune at US$1.7 billion.

Increased antitrust scrutiny from Chinese regulators has become increasingly common since the surprising halt of Ant Group's initial public offering last year.Tech companies including Alibaba, Tencent, Meituan and Pinduoduo have seen their once lofty valuations trimmed after being fined for reasons ranging from monopolistic practices to disrupting market orders to under-reporting deals.

At the same time, the Securities and Exchange Commission this month announced its final plan for a new law that mandates Chinese companies open their books to US scrutiny or risk being kicked off the New York Stock Exchange and Nasdaq within three years. That could mean hundreds of Chinese companies delisting from the US markets and relisting in Hong Kong or mainland China."The best days for China's tech sector are behind us for now," said Chen Zhiwu, director of the Asia Global Institute at the University of Hong Kong. "Without access to American capital markets, the history of China's tech sector would have been very different."

ByteDance founder Zhang Yiming is a rare Chinese internet tycoon to see his fortune grow this year, gaining US$19.5 billion based on a valuation in a SoftBank filing this year. That is partly due to his keeping the parent of TikTok a closely held company, insulated from the swings of market turbulence.But Zhang has also strived to keep a low-profile during the regulatory crackdowns. In May, he announced he was stepping down as chief executive and then quit the board last month.

Many executives made similar moves. Su Hua, co-founder of livestreaming app Kuaishou, ceded the CEO role in November only nine months after the company's IPO in Hong Kong. In September, JD.com named a new president, saying that chairman Richard Liu Qiangdong will focus on long-term strategies.Even with the loss in personal wealth, some have upped their philanthropy in response to President Xi Jinping's admonitions for "common prosperity" to address social inequality.

Xiaomi's Lei Jun and Meituan's Wang Xing have donated stakes worth US$2.2 billion and US$2.3 billion, respectively, to charity, which has partly contributed to their dented fortunes.Through the end of August, Chinese billionaires had donated US$5 billion to charity in 2021, 20 percent more than total national giving the previous year.

With iconic tech billionaires like Ma receding from public prominence, the industry needs to reshape its core strategy for new growth, HKU's Chen said."I think good days will return at some point after some soul searching and reassessment of what drove the golden days of the past two decades," Chen said.

BLOOMBERG