Read More

MPF funds flying the flags for China, Hong Kong and Asia have been pumping cash into booming American markets to boost earnings, putting unwitting investors at risk in more ways than one.

ADVERTISEMENT

SCROLL TO CONTINUE WITH CONTENT

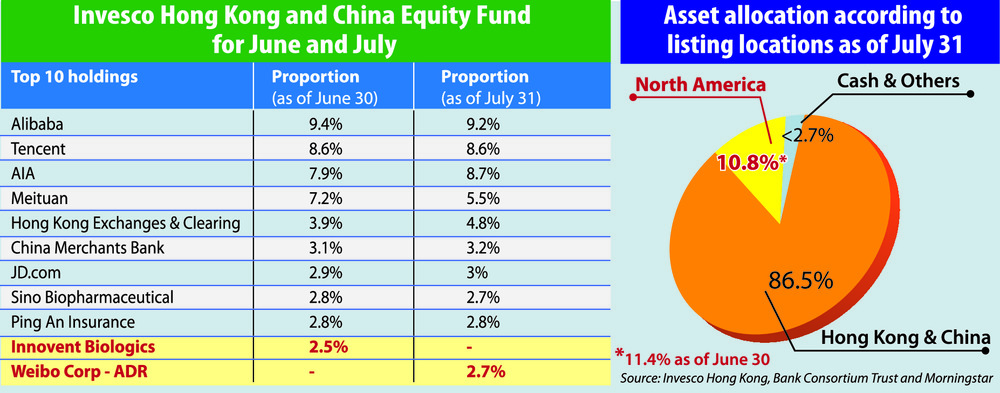

Ostensibly aimed at China and Hong Kong, a "Hong Kong and China Equity Fund" had in fact invested up to 11.4 percent of its portfolio in Northern American securities recently while an "Asian Equity Fund" at one point had 5.4 percent of its portfolio also invested in markets halfway across the world.

They are among 12 funds offered by Invesco, an American independent investment management company that is headquartered in Atlanta and a major provider of pension funds in Hong Kong.

Invesco's fact sheet says stocks bought by these two funds are "US-listed firms that pull in most of their earnings from Hong Kong, China and Asia."

Market watchers, however, say fund managers are being selective with the truth and inept in their fiduciary duty by not warning investors about the risks of buying Chinese stocks listed in America.

US-listed Chinese stocks have taken a battering in recent months amid Beijing's sweeping crackdown on big tech, private educators and the like - and the rout would have further driven these portfolios down.

Meanwhile, American sanctions against China and Beijing's tit-for-tat counter-sanctions could put MPF investors who invest in these funds in the cross hairs of US and Chinese regulators.

Critics say that at best, these funds demonstrate a lack of transparency. And at worst they could be breaching fair trade practice in Hong Kong, by not revealing the risks involved and painting the whole picture.

They also accuse the Mandatory Provident Fund Schemes Authority of turning a blind eye toward the fund managers and how they operate.

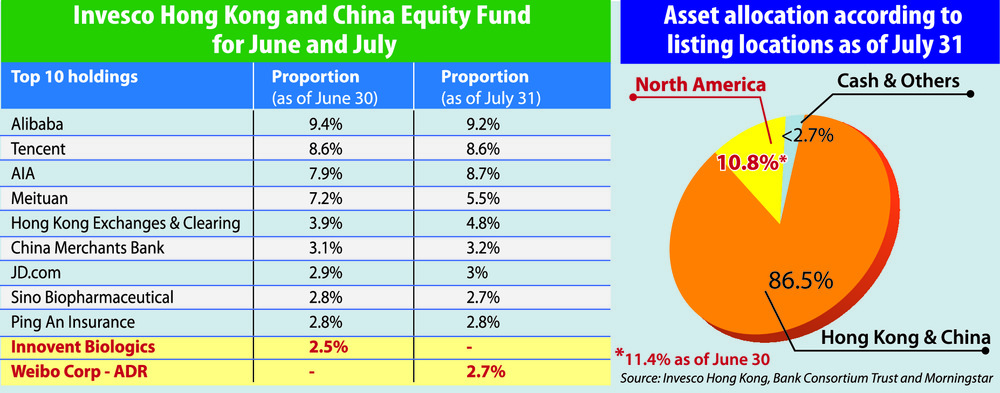

Hong Kong currently has 16 MPF "scheme sponsors," according to the MPFA. Some disclose asset allocations by sector but Invesco's are based on geographic locations. At face value, the name "Hong Kong and China Equity Fund" appears to suggest just that - a fund investing in Hong Kong and China equities.

Sraightforward enough, one would say.

But it's investment objective - "to achieve long-term capital appreciation through investments in Hong Kong and China-related securities" - clearly leaves the door open to interpretation.

However, there's much more than semantics that's at stake here.

Established in 2003, the fund today is worth in excess of HK$4.7 billion.

Back in November 2019, the Hong Kong and China Equity Fund had only 4.9 percent of its assets allocated to North American securities while the Asian Equity Fund had none.

But in January this year, the Hong Kong and China Equity Fund's North American assets was put at 9.4 percent and this number grew to 11.4 percent before coming down by less than a percentage point to 10.8 percent, according to its latest fact sheet, with the rest invested in Hong Kong and China equities.

The HK$1.62 billion Asian Equity Fund meanwhile had 5.4 percent of its portfolio in North America earlier this year from nothing in 2019, though this has now come down to 3.8 percent.

Analysts say these funds have been tapping into North American equities to bolster their returns as Hong Kong and China stocks languish behind their global peers - but at the expense of proper representation to the common man.

The benchmark Hang Seng Index is down more than 7 percent this year while markets in China have only risen between one and five percent.

In contrast, the three major US indexes - the Nasdaq, Dow Jones Industrial Average and Standard and Poor's 500 - have skyrocketed between 15 and 19 percent and are setting new records by the day.

The Hong Kong and China Equity Fund achieved returns of 2.17 percent in the first half of the year, but is now down nearly 10 percent year-to-date, after a July battering.

But the most recent lowering of these allocations show that the fund managers may be now thinking twice about North American securities.

When contacted by The Standard, Invesco was coy about what constituted "North American equities."

It only described "China equities" as "issuers generating a substantial portion of their revenues and/or profits in China listed in any exchanges."

The MPFA says the fund managers are going by the book. It points out that a fund titled "Hong Kong and/or China" can invest in shares listed overseas, as long as those firms have significant operations or derive a material proportion of their revenues in China and Hong Kong.

Critics however say it's time to throw the old rulebook out of the window as the ballgame has changed in light of the volatility that's hit US-listed Chinese stocks and the uncertainty over their future in those markets.

The rules allow MPF providers to invest in an array of mainland companies listed in the US as well as Chinese firms listed in the form of American depository receipts, including China's major telecommunications and oil giants.

Over the years, Corporate China has flocked to the US to cash in on an IPO gold rush, and as of May this year there were close to 250 of them listed on these US exchanges with a total market capitalization of US$2.1 trillion (HK$16.3 trillion).

But things have changed amid Beijing's regulatory crackdown wave and increasingly fractious relations between the rival superpowers. In early 2021, the US government slapped an investment ban on CNOOC, China Mobile, China Unicom and China Telecom among others, forcing them out of US exchanges. Meanwhile, around 17 Chinese firms have delisted from the US between last October and May, while a Forbes analyst has warned that stricter US disclosure laws could see up to 200 Chinese firms head for the doors.

But more to the point, Hong Kong's investors are still in the dark over whether Invesco has placed bets on these US-listed players and whether they are at risk, as its funds only list their "top 10" holdings.

Earlier this year, the "top 10" in the Hong Kong and China Equity Fund were all traded in Hong Kong and China, taking up to 51.2 percent of the portfolio with the top three - Alibaba, Tencent and AIA - commanding a little over a fourth of the total. The latest fact sheet, however, now shows one US-listed stock, Weibo Corp, in 10th place.

The remaining constituents are anybody's guess.

Other MPF providers - including BCT, HSBC, Manulife and AIA - are reticent to discuss where they are placing their money in terms of geography, sticking to allocations only by sector or industry.

Anli Securities chairman and chief executive Andrew Wong Wai-hong says investors should be wary of investing in US-listed Chinese stocks if funds managers shy away from disclosing the risks that go with it.

Fund managers have a fiduciary duty not to expose investors to unnecessary risks, he says, pointing out that people's life savings are at stake. He also puts the onus on the MPFA to review codes on disclosures and every registered fund's investment statement and objectives.

But loopholes exist.

If a fund's prospectus has no restriction on the investment proportion of certain assets, it does not violate any rules, says Billy Mak Sui-choi, an associate professor of the department of finance and decision sciences of Hong Kong Baptist University.

Hong Kong ushered in a Trade Descriptions Ordinance in 2013 with the vision of protecting consumers from unfair trade, but pension funds were not placed under its purview, as activities related to MPF businesses - "dealings of market intermediaries with consumers" - had been covered by the relevant laws and the codes of conduct issued or approved by the respective regulators, such as the MPFA.

And the Customs and Excise Department, which enforces the ordinance, has limited itself to checks on smaller firms that flout the law.

But eight years on, it might be time to expand the law and grant it oversight on MPF funds, says barrister Albert Luk Wai-hung. If a fund states it will invest all its cash in China and Hong Kong equities but buys stocks in North America, it may be violating fair trade practice, but no law has been flouted as such, because the MPF managers do not answer to the ordinance, he points out.

In response to The Standard's questions on asset allocations, the MPFA says "all the risk factors applicable to a specific constituent fund in the registered scheme should be listed, according to the Code on Disclosure for MPF Investment Funds, which was updated in December, 2019."

The Securities and Futures Commission declined to comment.

(This is a first in a series of investigative articles about the MPF that will be published by The Standard)