A flood of liquidity flowing into US markets in the past few months left many sensing that there is no end in sight to quantitative easing measures.

The standard yardstick for gauging the extent of the quantitative easing being undertaken is money supply. But the supply side does not show the other side of this financial equation: demand.

Only an interest rate can have both sides of this information embedded in it, from which the abundance of liquidity can be inferred accordingly.

The US Federal Reserve has rates targeted in a range of zero to 0.25 percent.

With this in mind, it carries out open-market operations by injecting liquidity into the Fed funds pool or extracting it so that the Fed funds' effective rate is in the target range, preferably near midpoint.

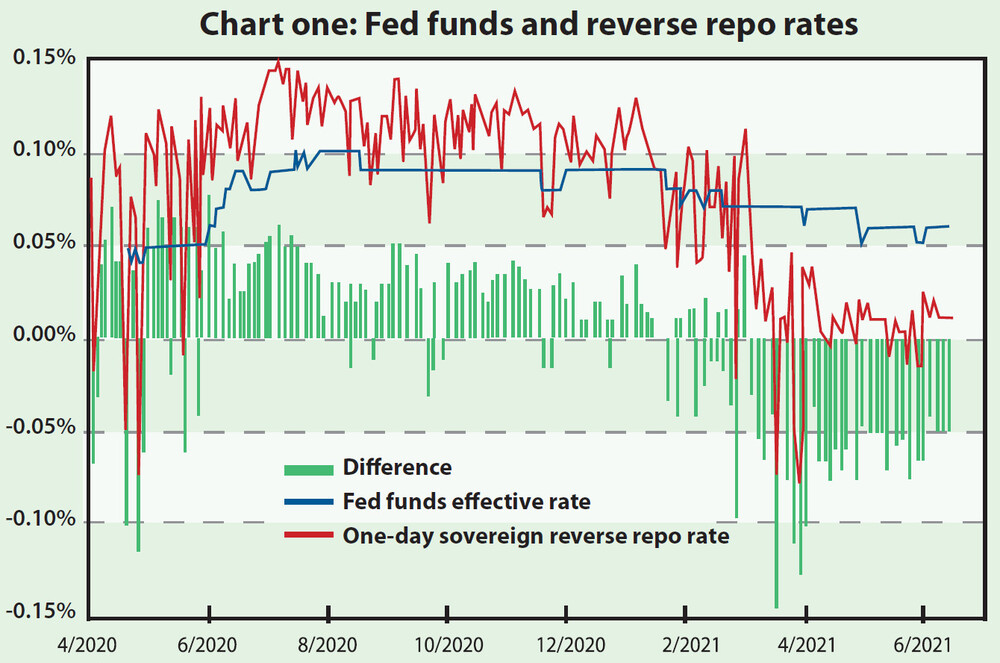

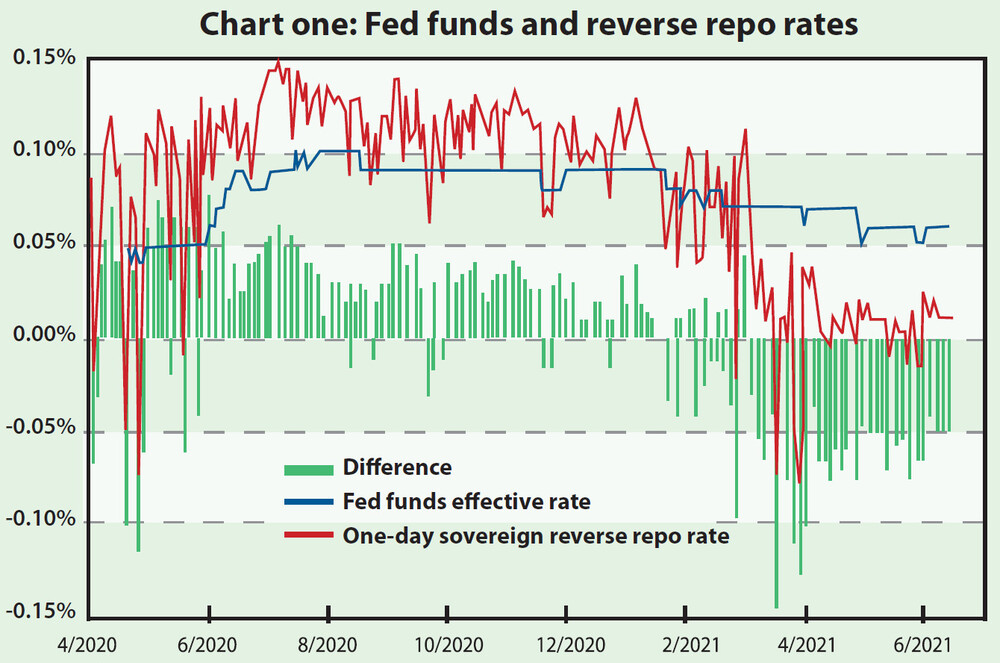

Chart one shows that Fed funds' effective rate has been lower than the midrange since an aggressive cut made last April.

The abundance has worsened between this January and April when the rate edged further down to 0.05 percent.

The reverse repo rate fell too.

The sovereign reverse repo rate used to be near the floor of the targeted range.

Years ago when the Fed hiked rates, it was a powerful tool for topping up all other rates, including the benchmark one.

The reverse repo rate currently fluctuates around zero (sometimes even below it), which suggests money is simply parked in a zero, or even a negative return, market without a good way out. This can be seen from the reverse repo rate falling faster recently than the funds' effective rate.

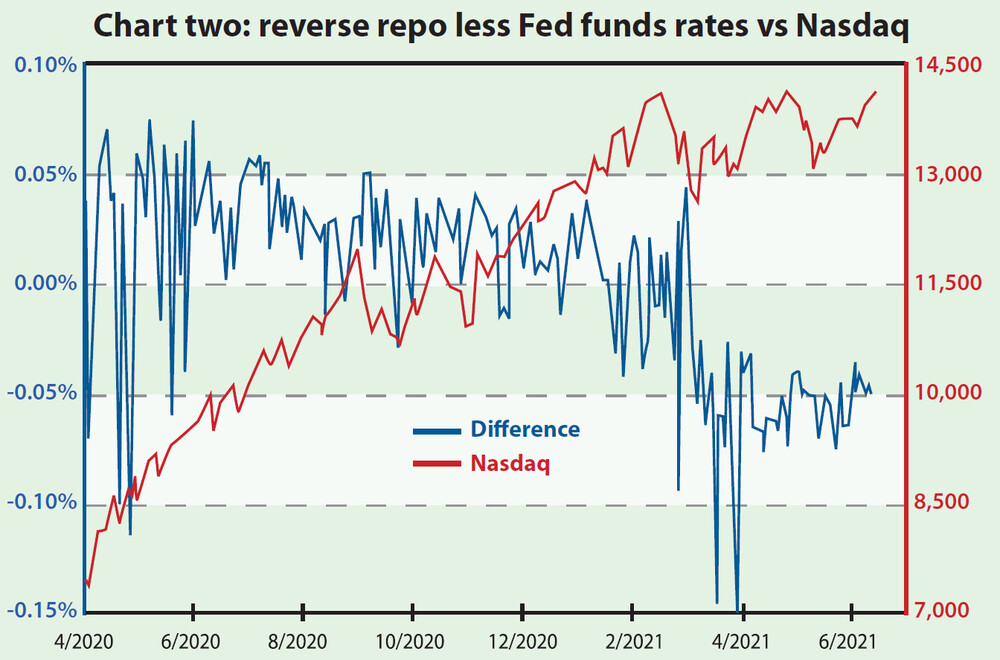

Chart two confirms this by comparing the reverse repo rate in discount of the Fed funds rate with the Nasdaq. The latter is used since it is sensitive to interest rates.

As such, we can see the Nasdaq turning flat as the reverse repo rate slides.

From then on, both remain at their corresponding levels.

The Fed has actually started tapering: both the monetary base and M2 growth have reduced significantly in April.

Law Ka-chung has worked in the financial industry and the government for two decades. Reach him at facebook.com/kachung.law.988 or lawkachung@gmail.com