A surge in long-tenor US Treasury yields and a rebound in the exchange rate of the US dollar has sparked worries over capital outflows from emerging markets.

Although Hong Kong is rich in a per-capita sense, it has often been regarded as an emerging market, especially since Beijing asserted direct control over it.

The exchange rate is a fast indicator of the flow of capital; it occurs real time around the clock.

Otherwise, one has to gauge the situation from monthly macro data, which is accurate but slow in coming.

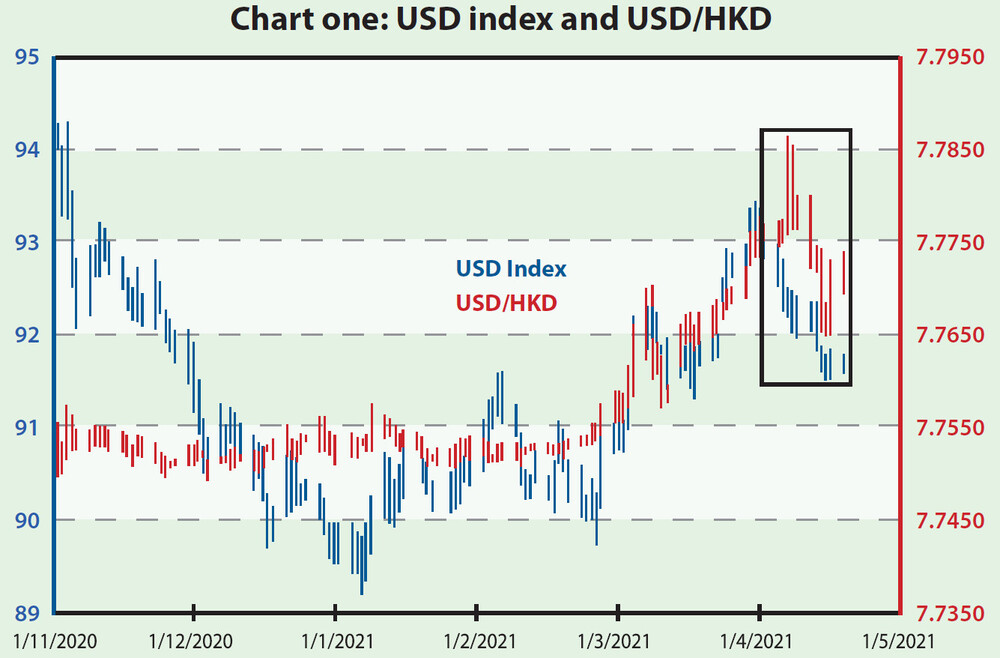

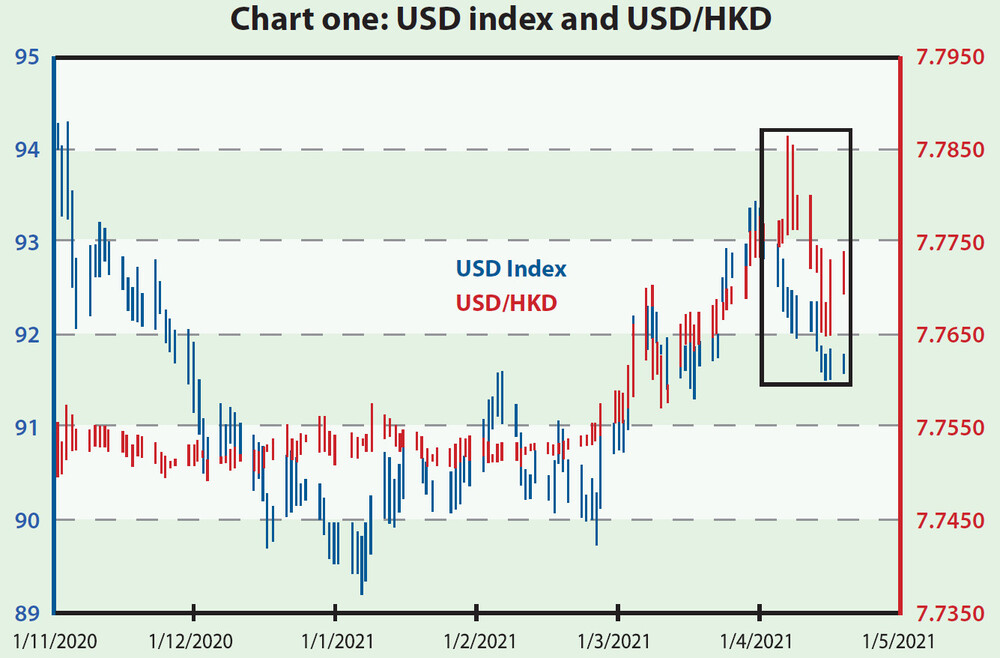

Since mid-February, when the Hong Kong stock market peaked, the HK dollar has weakened from 7.75 to 7.786.

The weakening in the exchange rate of the HK dollar could be due to a strong outflow trend, but it could also be due to the overall strength of the greenback.

If the dollar index goes up and brings USD/HKD higher, then the HK dollar's weakness is due less to such outflows.

From chart one above, we can see that such a connection has been true from mid-February to late March. Since this month, however, the US dollar has weakened and so has the HK dollar!

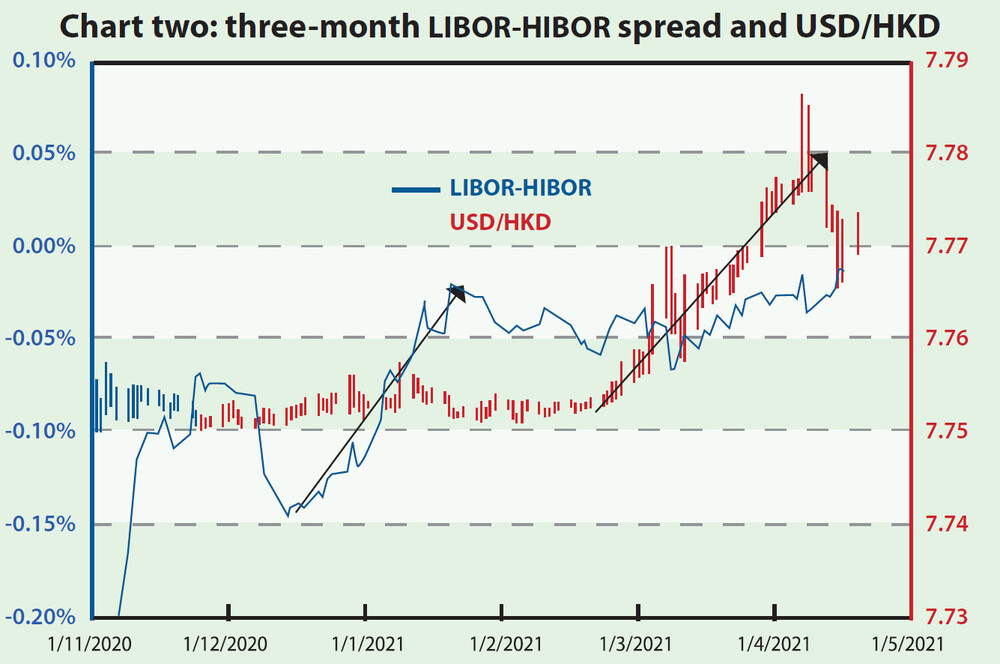

This means there should have been capital outflows at least in the first half of this month. To crosscheck this, we can utilize interest rate parity to compare the US-HK interest rate spread with the USD/HKD, where the two are expected to be proportional to each other.

The reason is simple: if there is a strong outflow trend, then the local interest rate, the Hong Kong interbank offered rate, will rise relative to the same tenor, implying a narrowing spread, while the USD/HKD will rise which reflects a weakening HK dollar. My previous study suggests interest rate spreads tend to move in advance. From chart two below we can see this is really the case.

Hong Kong is indeed experiencing an outflow.

Law Ka-chung has worked in the financial industry and the government for two decades. Reach him at facebook.com/kachung.law.988 or lawkachung@gmail.com