In an article entitled “Hong Kong as an International Financial Centre – Facts over Myths” posted in the Hong Kong Monetary Authority’s inSight column this month, chief executive Eddie Yue Wai-man tries his best to defend the position that there has been no net capital outflow from the SAR of late and that the situation actually involves the reverse case.

In a subsequent question-and-answer session, Yue defends the stance that there has been no recent substantial capital flight by pushing the argument that the Hong Kong dollar has been strong over the past year and that deposits have seen positive growth over the past two years.

It is very easy to see that such arguments are flawed.

First, exchange rate movements can be put down to capital flows, but they can also be shown to be simply the result of movements in the exchange rates of other currencies.

The US dollar index fell by more than 7 percent last year, and if we go back to its peak in March, that plunge widens to 13 percent.

All currencies would appreciate passively given this development and so this argument proves nothing.

Second, deposits growth can be fueled by an expansionist monetary base (ie, printing money), which will have a multiplier effect.

As gross domestic product generally grows over time in most countries, the money created for transactional needs has to grow accordingly.

So it would be a surprise if deposits are not growing over time, especially during a recession, when monetary easing is par for the course.

So this argument again proves nothing.

The HK dollar being pegged to the US dollar means, however, that if the Federal Reserve is printing money, the HKMA has to follow suit.

But this does not mean Hong Kong is attractive to foreign capital.

The government is twisting logic and trying to mask the truth by lying to the masses.

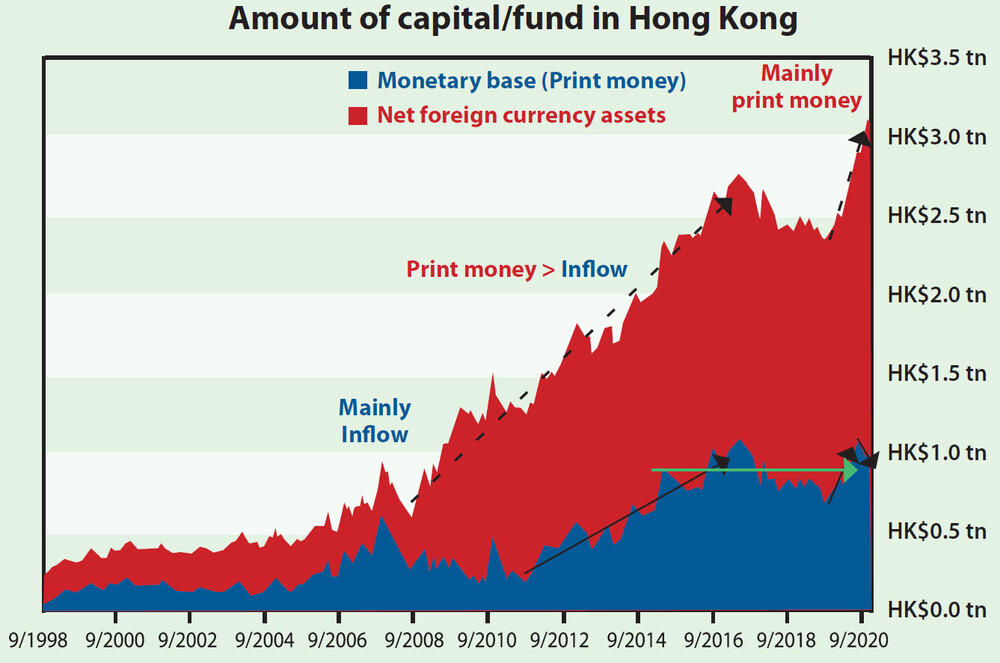

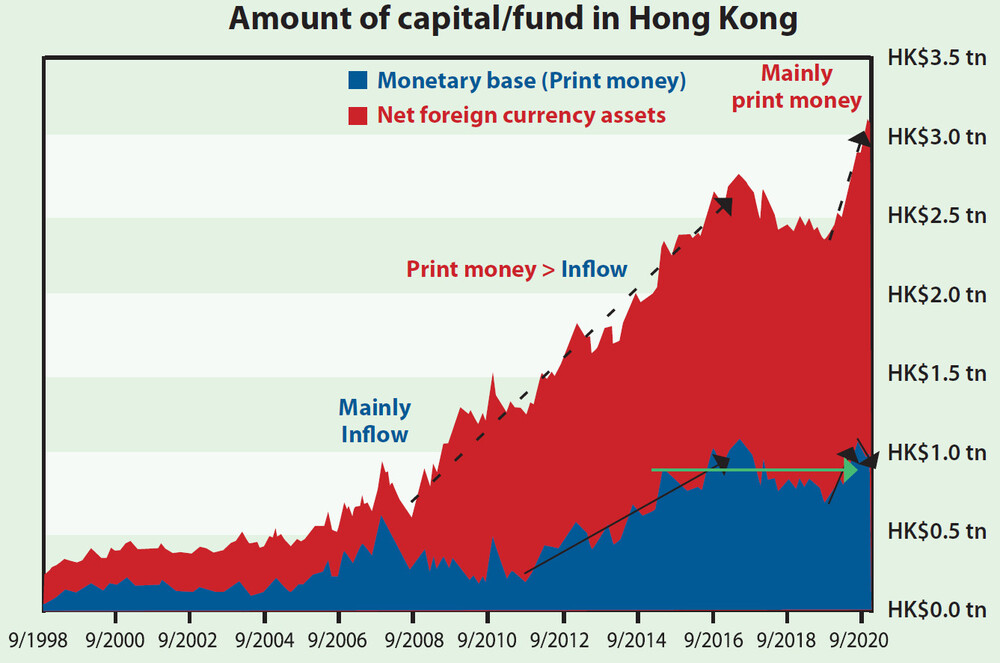

To see how they lie, let’s use their gold standard for capital measurements, suggested about a decade ago: the total amount in Hong Kong is the sum of locally printed money (the monetary base) plus net foreign currency assets.

Here the former is from local sources, with only the latter being from abroad.

An examination of the chart on top will lead one to easily conclude that it is locally printed money (in red) that is driving the total amount of capital in Hong Kong.

This is especially true over the past decade, with the HKMA following the Fed in ordering money to be printed at a much faster speed than the net influx of capital inflows (compare the dotted black arrow with the solid black).

A similar trend has been seen since the third quarter of 2019, and particularly noticeable has been the falling share of the foreign capital contribution, which has been falling from mid-2020 onward!

Ignoring the ups and downs, net foreign inflows have been showing a flat trend over the past five years (green arrow).

The stance that Hong Kong is continuing to be attractive to foreign capital is, as such, a lie to everyone.

Law Ka-chung has worked in the financial industry and the government for two decades. Reach him at facebook.com/ kachung.law.988 or lawkachung@gmail.com