The risk-on market since late-March goes hand in hand with the decline of the US dollar.

The logic behind it is simple.

When cash is turned into equity, there is selling pressure in the currency market.

As a result, the currency with the lowest interest rate is sold (short) to save costs.

In the past it was the Japanese yen, but nowadays most currencies pay zero interest. Thus, people simply sell the dollar.

Some say a democratic president favors a strong dollar.

This has been true since the Plaza Accord in 1985 and was true before the 1973 oil crisis, but was not quite the case between 1973 and 1985.

The era of Jimmy Carter saw a decline of the dollar index from 105 to 85, or 20 percent.

Meanwhile, in Ronald Reagan's first term in office ,the dollar index surged from 90 to its peak value at 165.

Thus, political party regime cannot explain the strength of the dollar despite every slump of the dollar being related to a political outcome.

For instance, the first time in 1971 was due to the collapse of the Bretton Woods system, where the dollar was no longer fully backed by gold.

The second time in 1985 was when the Plaza Accord was signed, in which Germany and Japan were forced to appreciate their currencies.

The third time in 2002 was when the G8 collaboratively rescued the euro by selling the US dollar.

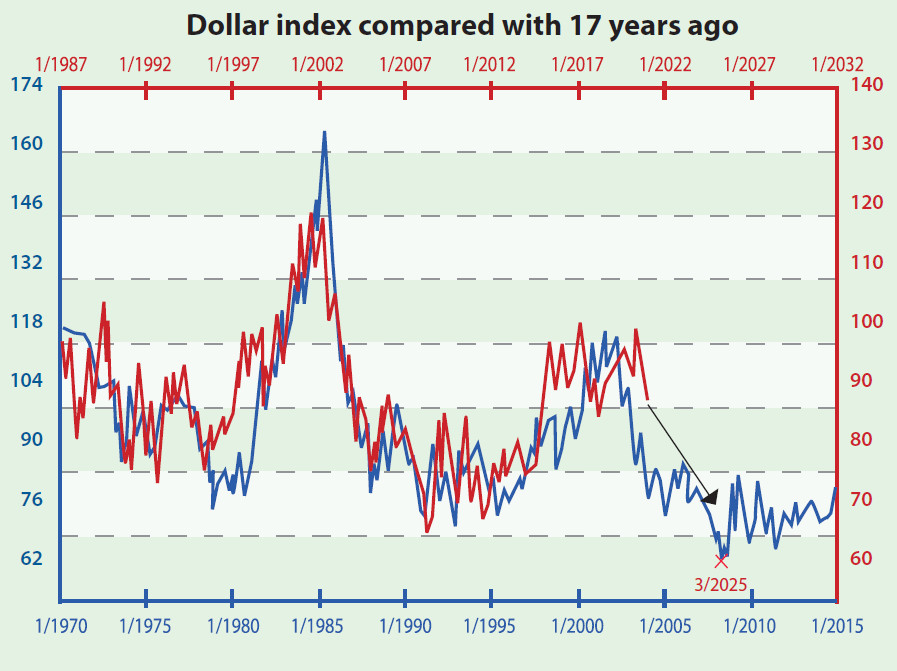

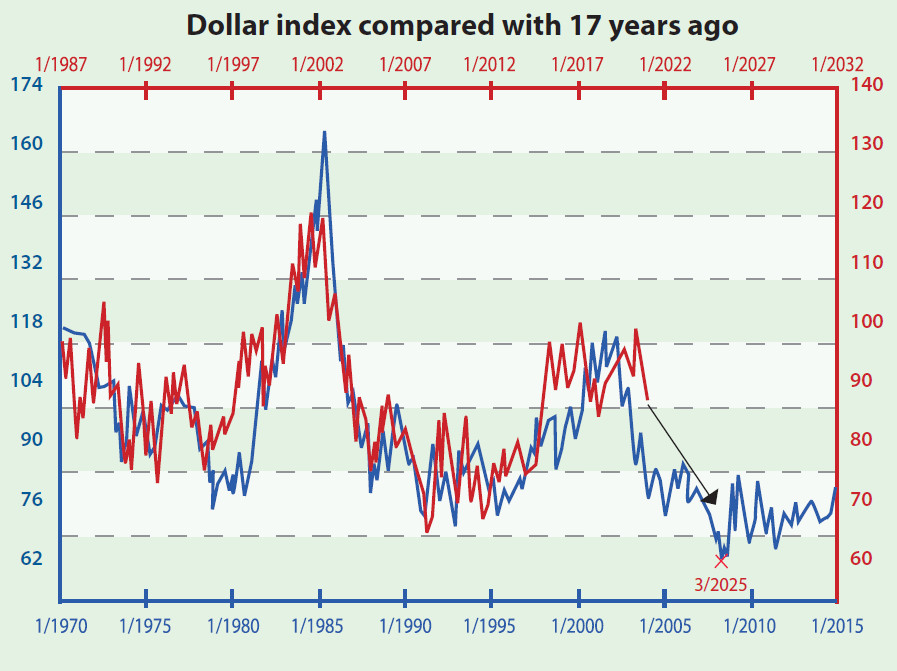

Incidentally, dollar ups and downs occur every 17 years as shown in the chart above. If the "coincidence" means the dollar index is replicating almost exactly the same path it charted 17 years ago, then such a "coincidence" has existed for too long - the blue and red lines (with a 17-year gap between them) overlap for a period of 34 years - almost since the record began.

Based on this, it should be clear that the dollar is undergoing another long bear market. It should not be surprising if the index level dips below 70 in five years or so.

Counting from the peak of 103, this means a total decline of 36 percent or an average of 8 to 9 percent per annum.

But this cyclical and regularly occurring pattern does not mean a decline of the dollar status.

The three historical episodes of such declines were not associated with a structural decline of the dollar's market share, whether in terms of the medium of transaction or the store of value.

The dollar still takes up over 60 percent of central banks' official reserves and for payments, the share is usually 40 to 50 percent.

So enjoy the upcoming risk-on era without worrying about the status of the dollar.

Law Ka-chung has worked in the financial industry and the government for two decades. Reach him at facebook.com/kachung.law.988 or lawkachung@gmail.com