Investors in the Hong Kong stock market must have found recent proceedings disappointing.

Indeed, as the Federal Reserve in the United States trimmed its interest rates down to zero with yet another round of quantitative easing, the country's stock market rebounded strongly, breaking record highs.

Hong Kong follows US monetary policy closely under its linked exchange rate system, but the Hang Seng Index saw only a dead cat bounce that ended by early July, two months earlier than in the United States.

The so-called strong inflow of funds into the SAR in the wake of a series of liquidity injections into the interbank market by the Hong Kong Monetary Authority might also be an illusion.

When the Hong Kong dollar's exchange rate to the greenback hits the lower bounds of 7.75, the Monetary Authority can intervene to bid up the rate by buying US dollars and selling the Hong Kong counterpart, which makes the process an injection.

However, even though the de facto central bank does not intervene, there will be other players in the financial markets who will, given that this is a sure-win trade.

Thus, the frequency and the quantum of the injection is arbitrary to a very great extent and should not be interpreted as an indicator of the flow of funds.

In fact, the three-month spread between the London interbank offer rate and its Hong Kong counterpart has widened from minus18 basis points to the minus 50 basis point level, which is by no means a signal that outflows have been occurring.

The recent correction that we have been seeing in the markets is doubtless a worldwide phenomenon, but most people are still hoping for developments that will bolster confidence.

These can take such forms as an effective Covid-19 vaccine becoming available soon, a tech breakthrough and probably further monetary easing measures to push up the stock market.

While technological optimism fueled a runup in Western markets, it's a nightmare here in Hong Kong with potentially more sanctions looming for mainland Chinese tech firms.

The worst factor is structural, which leads to irreversible damage to Hong Kong's stock market due to the structural decline of her Western system.

Hong Kong's role as an international financial center will also be gone, just like what Tokyo had experienced around two decades ago.

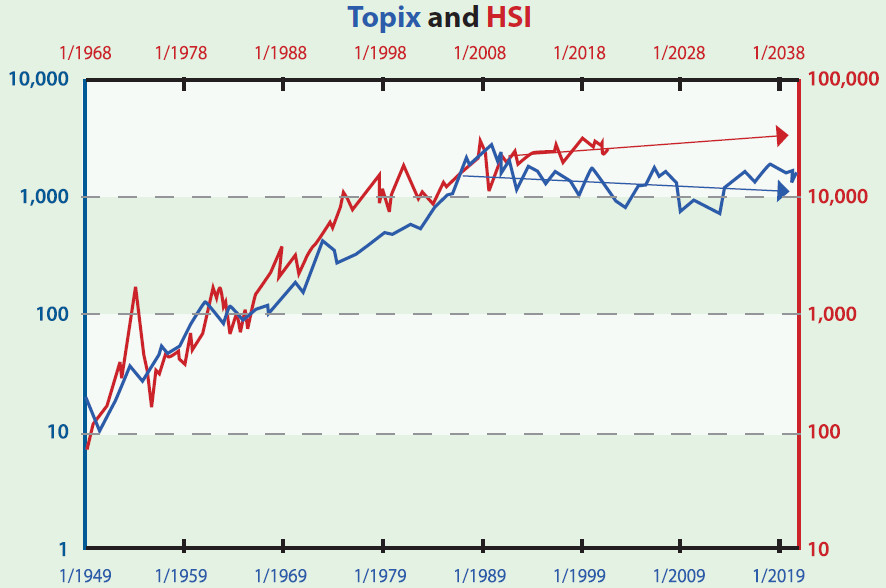

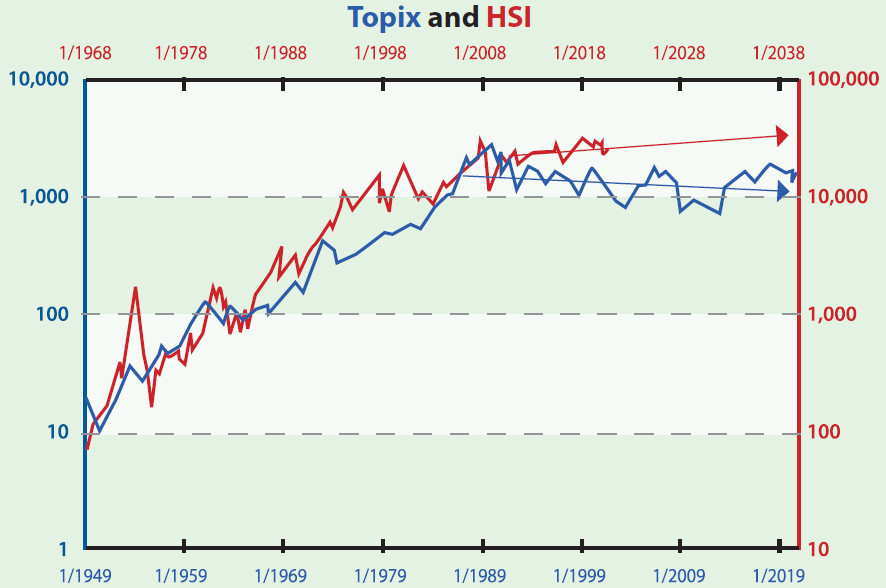

A comparison of the data on market capitalization and the annual fund-raising amounts brought in by the Tokyo and Hong Kong stock exchanges shows clearly that Hong Kong has been following in the footsteps of the Japanese bourse 19 years ago.

If a comparison is made of the two stock indexes, namely the Topix and the Hang Seng Index, we would see that the two take surprisingly similar paths, as the chart above shows.

Hong Kong seems to have a slightly better future, and that is probably thanks to the fact that its population aging is occurring to a lesser extent and its commercial sector is more flexible and efficient than Japan's.

However, the long-run outlook (a two-decade target) for the HSI is still gloomy, with a trend level only slightly higher than 30,000 points, which shows that the market has already peaked.

Law Ka-chung has worked in the financial industry and the government for two decades. Reach him at facebook.com/kachung.law.988 or lawkachung@gmail.com