By Haitian Lu, Yicheng Sun and Shan Huang

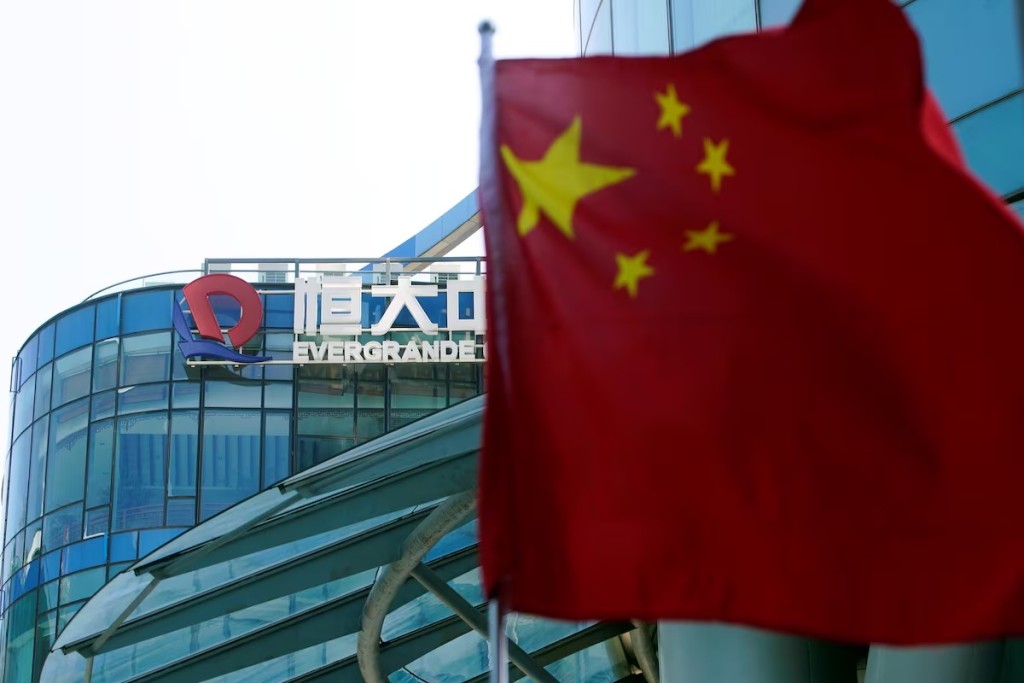

When China’s real estate giant Evergrande defaulted in late 2021, it sent shockwaves through global financial markets. But the fallout extended beyond the company itself. PricewaterhouseCoopers, Evergrande’s long-time auditor, soon found itself at the center of a credibility crisis.

In September 2024, China’s Ministry of Finance and the Securities Regulatory Commission concluded that PwC had failed to meet professional auditing standards and played a role in concealing Evergrande’s financial misstatements.

The penalties were historic: a 441 million yuan (HK$479.46 million) fine, a six-month suspension of PwC’s audit license in the mainland, and the closure of its Guangzhou branch. The scandal has not only shaken trust in one of the world’s most prominent accounting firms but also raised urgent questions about audit integrity and regulatory oversight in China.

Blow to PwC’s prestige

PwC, one of the “Big Four” global accounting firms, has long symbolized auditing excellence. Its name alone has often reassured investors and helped companies lower their cost of capital. But this scandal echoes past corporate disasters, such as Arthur Andersen’s downfall after Enron in the United States and ChuoAoyama’s collapse in Japan after the Kanebo case.

Our research shows that PwC’s reputation has suffered serious damage in China. We studied the performance of PwC-audited companies listed on China’s A-share market during key events related to the Evergrande case. Whenever new information emerged indicating PwC’s negligence, these companies experienced more severe stock price declines compared to those audited by other Big Four firms (Deloitte, Ernst & Young and KPMG). This suggests growing investor skepticism about the reliability of PwC’s audits.

Beyond a loss of clients

The impact was not limited to PwC’s direct clients. Our analysis found a spillover effect: companies audited by other Big Four firms also saw negative market reactions, showing that the scandal cast doubt on the wider auditing industry.

Furthermore, the damage extended within PwC’s own network. Clients of PwC’s Guangzhou office — the team responsible for auditing Evergrande — suffered more than those associated with PwC offices in other regions. Even nearby offices felt the ripple effect, reinforcing the idea that reputational harm can be both brand-wide and geographically concentrated.

Another troubling sign was a marked drop in what economists call earnings response coefficients — or ERCs —a measure of how much investors trust and react to a company’s reported earnings. PwC clients saw a sharper decline in ERCs than those of other firms, meaning investors began to discount the credibility of their financial disclosures.

We also found that newly listed companies audited by PwC lost one of the key benefits usually provided by Big Four auditors: lower financing costs. This indicates that PwC’s damaged reputation now hampers its clients’ ability to raise capital efficiently.

Why the reaction in China was so strong

In markets like the United Sates, audit failures often end in class-action lawsuits and large settlements. But in China, investor protection is largely built on administrative penalties, not court rulings. That means public trust plays a much larger role in maintaining market stability.

When Evergrande first defaulted in 2021, the share prices of PwC-audited firms showed no significant reaction. But as regulators revealed the extent of PwC’s role in the misconduct, market confidence eroded sharply. This shift highlights how investor trust — once lost — can have far-reaching consequences.

An audit firm’s name is more than a brand; it is reputational capital. And once that capital is compromised, it can shake confidence across the financial system.

The path to restoring trust

The scandal exposes serious weaknesses in China’s regulatory and legal frameworks. While the fines and suspensions send a strong signal, they may not be enough to rebuild investor faith.

China must strengthen its legal infrastructure, especially by improving class-action mechanisms that allow investors to seek compensation. Auditors themselves must recommit to the core values of integrity, independence, and transparency — regardless of client pressures.

Investors, both local and international, should also be cautious: being audited by a Big Four firm is no longer a guarantee of quality. Active oversight and due diligence are more important than ever.

Trust is the market’s lifeblood

Trust is the invisible currency of financial markets. It takes years to build, but only moments to lose. In places like China, where information gaps between companies and investors can be wide, the role of trustworthy auditors is even more critical.

The scandal has not only bruised PwC’s reputation but also revealed systemic vulnerabilities in China’s capital markets. Let this be a wake-up call: without accountability and reform, even the most prestigious names can fall short — and drag the market down with them.

Professor Haitian Lu is the Hong Kong SustainTech Foundation Professor at the School of Accounting and Finance, and a core member of the Policy Research Centre for Innovation and Technology (PreCIT), Hong Kong Polytechnic University.

Yicheng Sun is a PhD candidate at the School of Accounting and Finance, Hong Kong Polytechnic University.

Dr Shan Huang is a postdoctoral fellow at the Shenzhen Research Institute and the Policy Research Centre for Innovation and Technology (PreCIT), Hong Kong Polytechnic University.