High inflation should force the US Federal Reserve to start tapering, but chairman Jerome Powell uses the employment situation as a habitual excuse to defer it.

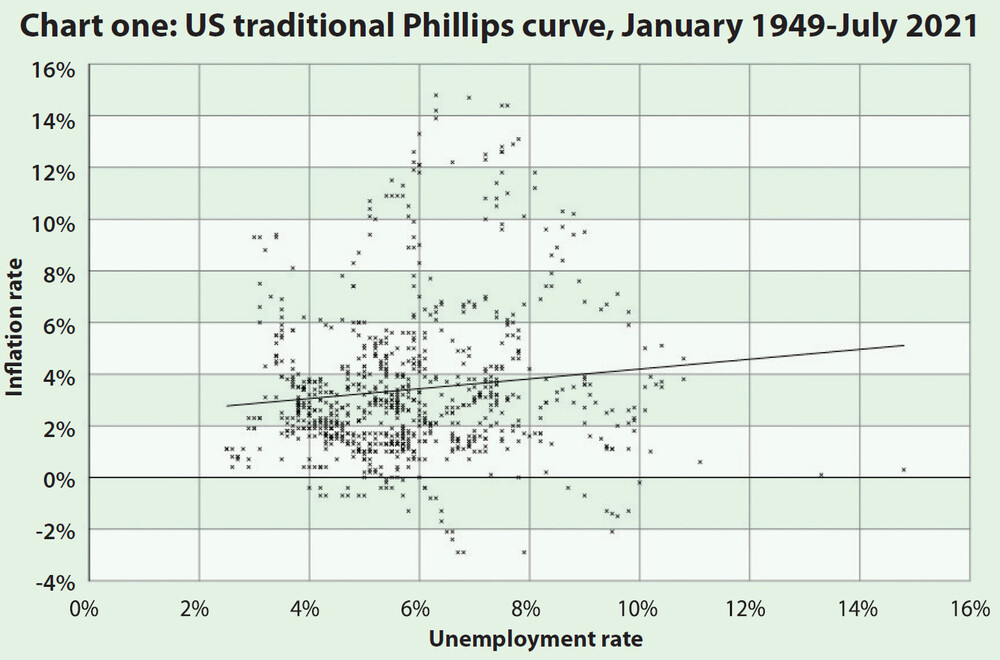

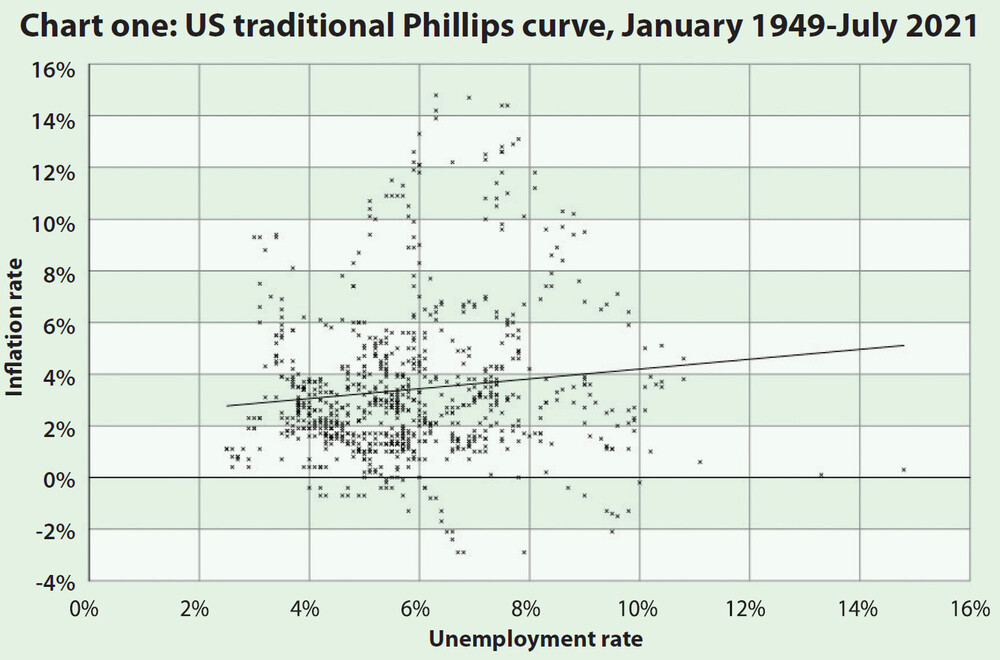

A traditional belief that full employment pushes up inflation is based on empirical results from the Phillips curve, which is the inverse relationship between the two discovered by A W Phillips in the 1950s. But academics have doubted this in recent decades.

The neoclassical stream offers strong doubts by suggesting the nominal variable (inflation) should not be dependent on the real one (unemployment) in the long run. That is, inflationary (accommodative) monetary policy cannot alter real activities by cheating forever.

Such a long-run failure hypothesis suggests the curve is vertical in the long run. Computing repeated regressions between inflation and lagging unemployment rates shows that the slope between the two is getting steeper as the lag increases from zero to three years.

This implies we shouldn't see a meaningful relationship between them in the long run. In fact, chart one verifies this as the scatter plot between them fits a pretty flat trend line.

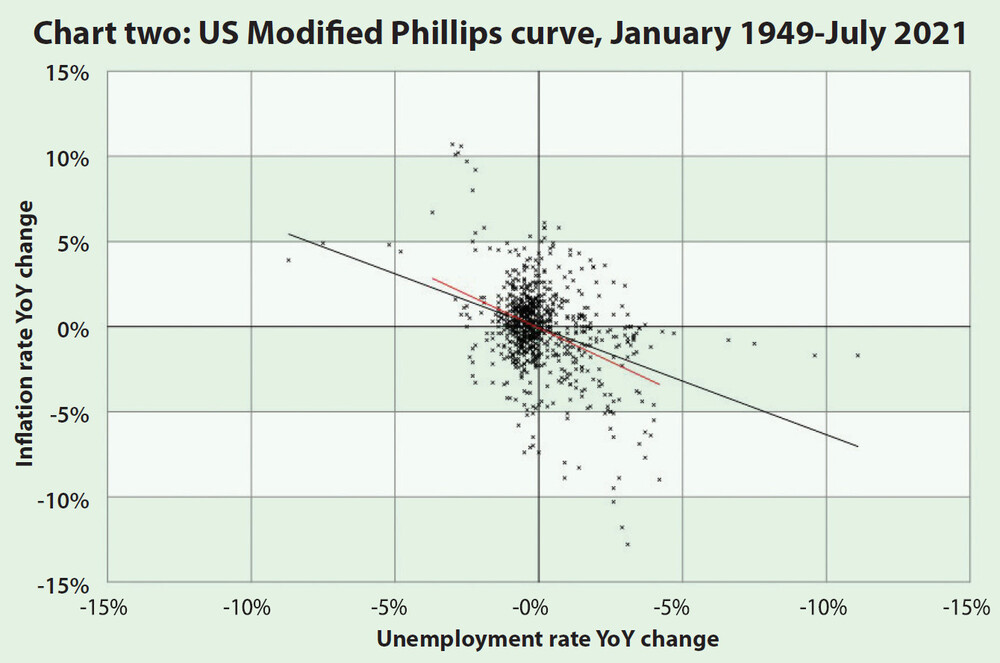

However, my contribution would be the introduction of a "modified Phillips curve" by taking growth rates on both variables.

Chart two shows (monthly) inflation changes over the previous year against jobless rate changes fits a much better negatively sloped trend line. Excluding outliers due to Covid-19, a similar but slightly steeper red line is obtained.

The reason for such a success is because chart two is essentially a deviation of chart one. Such a detrending way makes the business cycle components of inflation and unemployment sharper without altering the original relationship because the slope of the curve is preserved by taking a derivative on both variables (the derivative is a year-on-year change).

By employing such a small trick, the original curve relationship can reemerge!

Law Ka-chung has worked in the financial industry and the government for two decades. Reach him at facebook.com/kachung.law.988 or lawkachung@gmail.com