Mainland high-yield wealth management products are expected to attract Hong Kong investors given the interest gap between the mainland and local banks, while analysts also forecast diverse Hong Kong investment products would also drive southbound purchases through the Wealth Management Connect (WMC) in the long term.

The cross-boundary pilot scheme in the Guangdong-Hong Kong-Macao Greater Bay Area, announced on June 29, was rumored to set up a quota of 150 billion yuan (HK$164 billion) each for north and south investment flows, respectively. The individual credit limit is believed to be one million yuan.

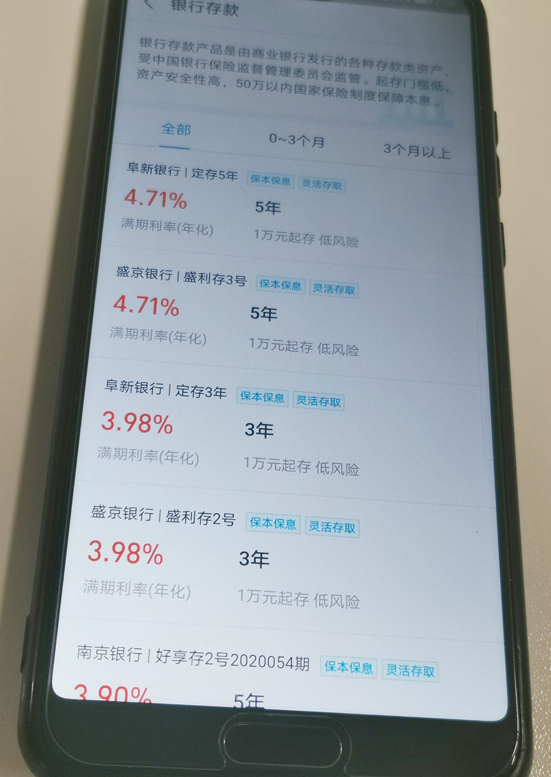

Terence Chong Tai-leung, an associate professor of economics at the Chinese University of Hong Kong forecasts mainland savings products with guaranteed annualized return rates of 4 percent or above are more attractive to Hong Kong investors.

Compared with Hong Kong time deposits, providing less than 1 percent interest rate, they are very attractive, he says.

Mainland banks, in general, provide structured deposit, principal-guaranteed wealth management products that target money market funds and government bonds, fixed-income products, as well as high-yield packaged products of corporate bonds and special loans. The return of the products is overall higher than that of those developed by Hong Kong banks, analysts say.

Around 50 percent of nearly 330 mainland wealth management products on sale this month reported an expected yield of 2.5 percent or above, according to data from mainland financial website Hexun.

Separately, Bank of China (3988) provides medium-risk wealth management products such as "Zhongyinzhaifu" and "Zhongyinwenfu", which invest in treasury bonds, local bonds, and corporate bonds. The products are available online and have a six-month expected return of around 4.5 percent.

The one-month Hong Kong Inter-bank Offered Rate was at 0.39929 percent last Friday while the comparable Shanghai Interbank Offered Rate stood at 2.0350 percent.

Apart from guaranteed return products, Chong says it is unnecessary for Hong Kong investors to buy mainland foreign currency products as they can buy them in the city. Also, products with stocks or corporate bonds as underlying assets are not expected to be popular, too, as there are also many choices in the SAR.

For mainlanders, Goldman Sachs expects Hong Kong's wealth management products would meet mainlanders' needs to build a diversified portfolio and to hedge exchange rate risks, but the scale of southbound flows would be smaller.

Apart from time deposits and certificates of deposits, major Hong Kong banks like The Hongkong and Shanghai Banking Corporation and Hang Seng Bank (0011) have developed more equity-linked investments and foreign exchange related products, which are not available for mainland investors now.

Market watchers estimate that the WMC may include simple investment products that have relatively low risks when initiated.

For Hong Kong banks, analysts from UBS Global Wealth Management Chief Investment Office say that the launch of WMC would bring higher sales and wealth-management revenues, which make up around 10 to 15 percent of their total incomes.

Greg Hingston, regional head of wealth and personal banking of Asia Pacific at HSBC added: "GBA is one of the world's largest banking clusters with expected banking revenues to reach US$185 billion (HK$1.44 trillion) by 2025, a 10.3 percent compound annual growth rate."

But analysts from UBS warn that these incremental revenues may not make a meaningful impact in the near term, given recent headwinds, such as falling net interest margins and rising credit costs.

Hong Kong investors may be concerned about a repeat of the "Yuan Yao Bao". Investors of the speculative crude oil futures product of Bank of China even had to pay back over 5.8 billion yuan of margin due to negative oil futures prices in April.

Chong warns that all investments have risks and Hong Kong investors should take the fluctuation of the yuan into consideration amid the market volatility.

Mainland banks have always used "low risk and high returns" as selling points for their products but investors should be careful about the product types, market watchers say. Products tracking glass futures, eggs, and even Pu'er tea have been launched by mainland banks.

KPMG suggests that financial institutions should focus on risk tolerance and qualification of investors when designing the products, and that sales agencies must clearly explain to customers the protection of investors' rights in different regions in the GBA.

Analysts also note it may take some time for the WMC to become popular, which has been seen in the Stock Connects and the Mainland-Hong Kong Mutual Recognition of Funds.

The Stock Connects recorded its highest turnover for both sides' trading on July 6, with a northbound trading volume of 172.7 billion yuan and a southbound volume of HK$60.2 billion, using only 15.8 percent and 13.3 percent, respectively, of daily quota for each side of flows, HKEX data showed. Also, the accumulated sales of Hong Kong funds that were approved to be sold in the mainland had only used 16.71 percent of a 300 billion yuan quota as of May 31 since the fund recognition was launched five years ago. The figure for mainland funds sold in Hong Kong was only 0.49 percent of the quota, according to the State Administration of Foreign Exchange.