Read More

The S&P 500 closed at a record high on Tuesday, wiping out losses from the coronavirus-induced sell-off and returning the market to pre-pandemic levels, CNBC's Nate Rattner writes.

ADVERTISEMENT

SCROLL TO CONTINUE WITH CONTENT

But while the index is right back where it started before the virus sent the market plunging, a CNBC analysis shows that the majority of stocks have yet to climb back to their prior levels. While the overall market crashed and then reached new heights between its previous high on February 19 and new high on August 18, only 38 percent of stocks in the index made gains over that time period. A majority, the remaining 62 percent, were negative.

In many cases, these still-reeling stocks are down significantly from where they were in February. While there have been a number of big winners — 43 stocks in total saw gains of 25 percent or more, including health care and technology names like ABIOMED (87 percent), PayPal (57 percent), and Amazon (53 percent) — there have been far more big losers.

A quarter of the index, 126 stocks in total, recorded declines of 25 percent or more compared to the February 19 starting point. Norwegian Cruise Lines (-71 percent), Occidental Petroleum (-67 percent), and Carnival Corporation (-67 percent) are the top three laggards over the period.

In an interview on CNBC following Tuesday’s record close, Michael Yoshikami, CEO of Destination Wealth Management, described a “shift in demand” that explains why stocks haven’t moved in unison since the market’s last record.

“It’s not as if everything is rising,” he said. “You pull money out of names that really aren’t attractive given current conditions. And that money moves over to companies that are thriving in this environment.”

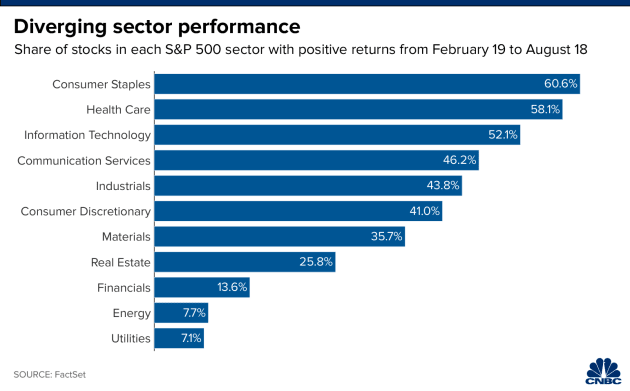

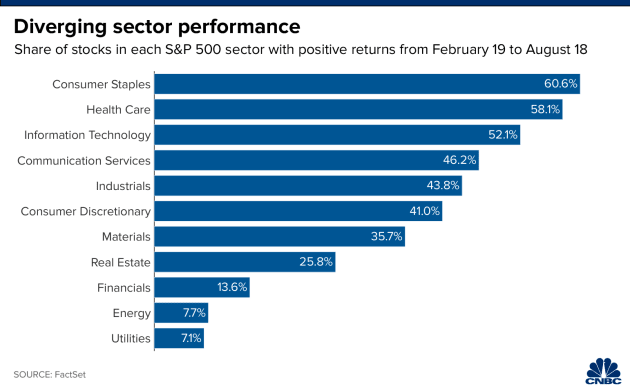

As Yoshikami described, stocks in some sectors have fared better than others. In consumer staples, health care, and information technology, more than 50 percent of stocks posted gains between February 19 and August 18. In energy and utilities, however, less than 10 percent did so.

But even within individual sectors, performance has not been uniform. Tech stocks, for example, which climbed by 12 percent from prior high to new high and are an oft-cited explanation for the stock market’s incredible comeback, saw wide-ranging performance. On one end of the spectrum, PayPal and Nvidia each gained by more than 50 percent while on the other end Western Digital and Xerox both fell just as steeply.

In the health care sector, performance varied just as widely. Abiomed led all stocks in the index with an 87 percent gain from February 19 to August 18, and West Pharmaceuticals and Regeneron, at 58 percent and 54 percent, were also among the top performers. But more than 40 percent of stocks in the sector were down, including Dentsply Sirona (-26 percent), Universal Health Services (-19 percent), and Cigna (-18 percent).

The one area in which stocks have shown alignment is throughout the market’s return from the S&P 500′s March 23 low point, when the index grew by 52 percent en route to the new record high. Over that surge, just six stocks — Coty Inc., FirstEnergy, Walgreens, Gilead Sciences, Wells Fargo, and Intel — were negative.