Read More

Morning Recap - July 22, 2026

57 mins ago

Deborah Lee breaks silence after Patrick Tse’s death

20-07-2026 21:00 HKT

Alibaba Group founder Jack Ma Yun has been spotted in Hong Kong - almost a year after regulators pulled the plug on Ant Group's initial public offering.

Two highly-placed sources told The Standard that they saw Ma in the city on October 1, months after he laid low in the mainland away from public limelight.

While Ma has appeared in several mainland events since the beginning of this year, it was the first confirmation that he came to Hong Kong amid rumors that he was banned from leaving the country.

It is unclear who Ma met with during his time in Hong Kong and whether he has since left the city.

Ma's appearance is considered a benchmark of the tech giant's relationship with mainland authorities.

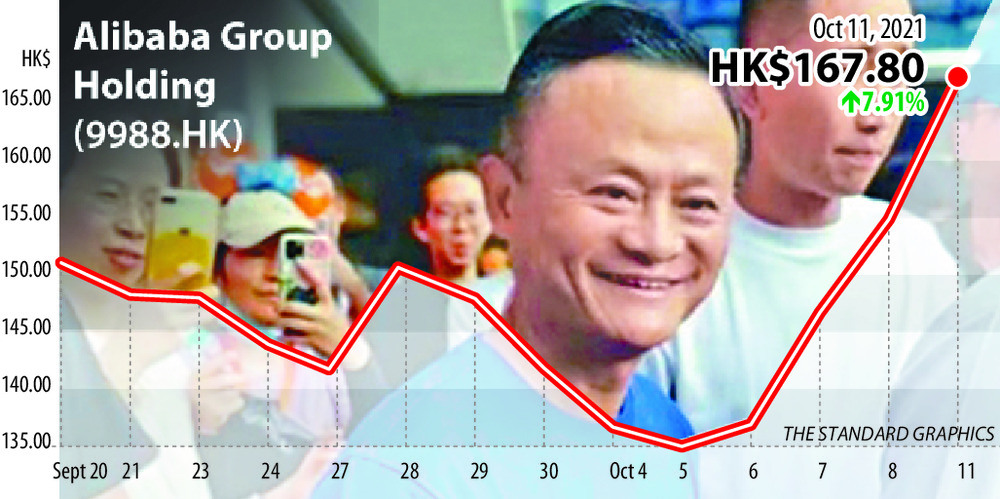

Coincidence or not, Alibaba (9988) shares went up 18 percent from HK$142.2 on September 30 to HK$167.8 yesterday.

The surge exceeded that of other tech heavyweights such as Tencent (0700), whose shares increased by 7.49 percent to close at HK$496 during the same period.

Relations have been warming up as Alibaba invested into making the hugely popular patriotic movie The Battle of Lake Changjin. The company also made commitments to back President Xi Jinping's "common prosperity" initiative to narrow the wealth gap.

Alibaba Pictures Group is among 17 production companies that invested in the war epic that shattered worldwide box-office records.

The patriotic movie talks about China's battle against US forces in the Korean War. Reportedly costing over 1 billion yuan (HK$7.8 billion), the movie has already grossed more than 4 billion yuan since it debuted on September 30. It is set to be China's and the world's top-grossing movie this year.

In comparison, the new James Bond movie No Time to Die has grossed US$313 million (HK$2.4 billion) since its international release two weeks ago.

Alibaba will invest 100 billion yuan into Xi's common prosperity initiative by 2025, offering subsidies for small and medium-sized enterprises and improving protection for workers such as couriers and ride-hailing drivers.

Mainland regulators pulled the plug on the initial public offering of Ant Group, an affiliate of Alibaba Group, in what could have been the world's largest -ever IPO in November 2020. The Hong Kong leg of its dual listing was also put on hold.

The IPO was called off shortly after Ma criticized the financial regulators and banks in a forum in October last year, saying the regulatory system stifled innovation and must be reformed to fuel growth.

Since the IPO was halted, Ma almost disappeared from public view, prompting reports that he had gone "missing."

He reemerged in January in a video uploaded to social media, where he addressed mainland rural teachers in an initiative under his charity foundation.

After Alibaba was fined a record 18.2 billion yuan by the antitrust regulator in April this year, Ma attended an event at Alibaba's headquarters in Hangzhou in May to thank employees' family members.

With pictures of Ma circulating on the internet, netizens were quick to point out he had gray hair strands and seemed to look older.

Joe Tsai Chung-hsin, Alibaba's executive vice chairman, gave reassurances that Ma was well. He said Ma focused on hobbies and philanthropy while keeping a low profile.

"He's actually doing very, very well. He's taken up painting as a hobby. It's actually pretty good,'' Tsai said.

Ma's last appearance was when he visited a farm run by Alibaba in Zhejiang province on September 1. A day after, Alibaba announced its 100 billion commitment into "common prosperity."

Yesterday, Hong Kong shares rose to end at a nearly four-week closing high as Alibaba and Meituan ( 3690) rallied, with investors rushing to buy on bets that crackdowns against tech giants are nearing an end.

China's antitrust regulator fined Meituan 3.4 billion yuan for abusing its dominant market position - a smaller amount than expected.

The Hang Seng Index closed at 25,325, up 1.96 percent. Alibaba shares gained 7.91 percent from last Friday.

Meanwhile, Ant Group has raised its registered capital to 35 billion yuan from 23.8 billion yuan, public business registration records showed, as the fintech giant continues its government-mandated restructuring since April.